- Fixed-rate sales commission: Their bank get allows you to move your varying interest rate into the a fixed rate of interest however, commonly charge a fee to help you exercise.

The three-time cancellation laws

After you have closed new contract to open a good HELOC, which federal code will provide you with about three business days, in addition to Saturdays (yet not Sundays), to help you cancel this new arrangement unconditionally in the place of penalty.

The three day termination period starts just whatsoever ones the unexpected happens: you have finalized the mortgage within closure, acquired a reality for the Financing disclosure setting with what of the borrowing from the bank contract, and you can received several duplicates of Information inside the Lending see that define your own straight to cancel.

Brand new termination period comes to an end at nighttime towards the 3rd go out shortly after the past of a lot more than criteria happen. Including, for individuals who finalized the borrowed funds contract and you may received happening in the financing revelation mode to the Wednesday but don’t have the two copies of one’s right to cancel notice up to Monday, you have up to midnight Saturday to cancel.

Remember that you will not found the means to access the fresh HELOC until once the three months possess passed. You may not owe any costs for many who terminate from inside the three time months, and you will be refunded one charge currently repaid.

Discover a long list of the three day cancellation rule along with your legal rights since the a homeowner when obtaining an effective HELOC on the Government Trade Fee website.

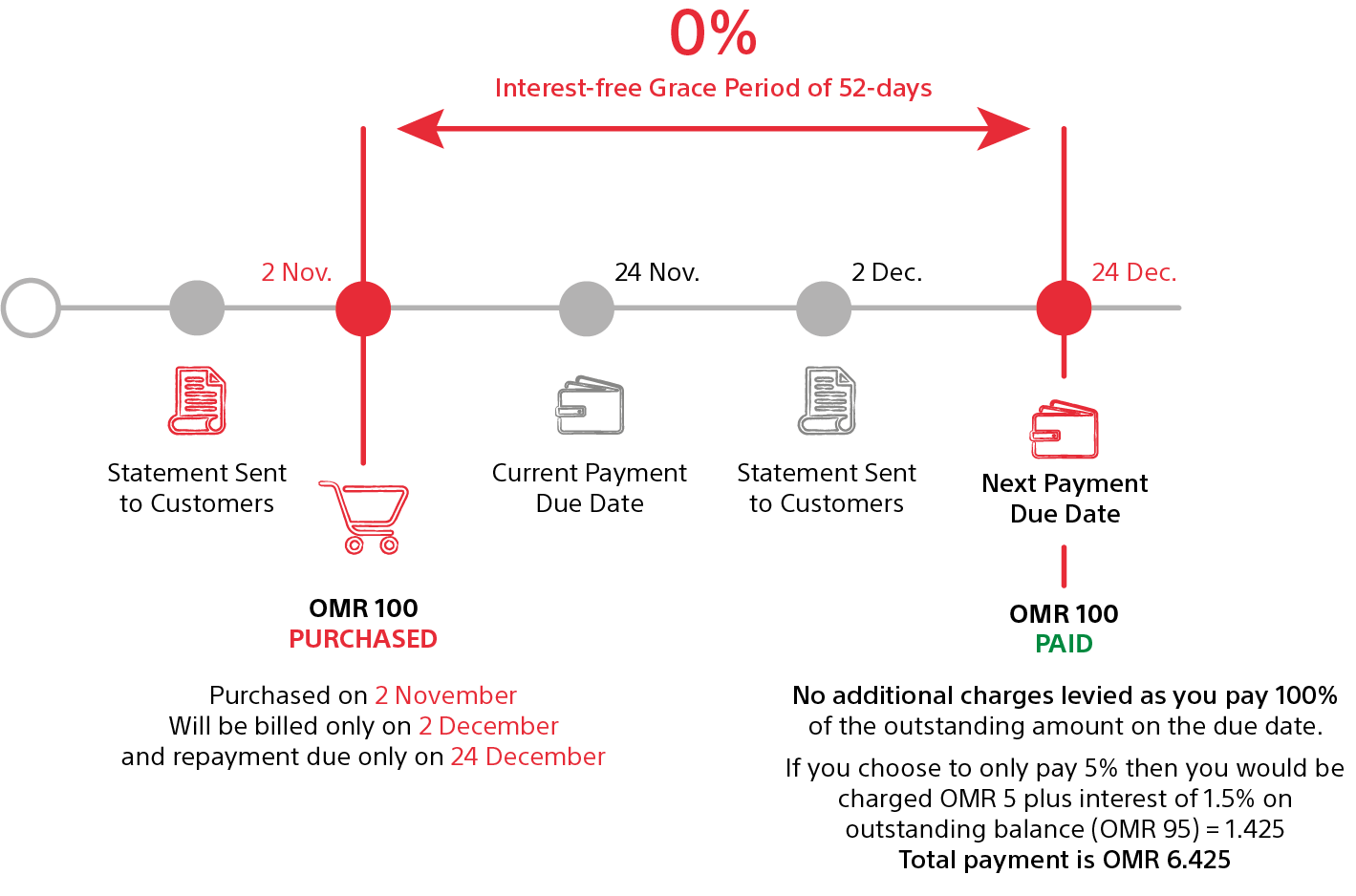

how to get a 300 loan with bad credit

Harmful techniques

Since your family serves as equity to own good HELOC, it is essential to find an established lender and give a wide berth to deceitful practices that will end in a pricey misstep.

Mortgage turning occurs when the bank prompts that several times re-finance the loan, that can make you acquire extra money than simply expected. Additionally spend the brand new settlement costs and you may charges any time you re-finance.

Lure and option is when the financial institution has the benefit of one to selection of terms and you may cost after you incorporate next alter them otherwise pressures your towards acknowledging various other terms when you indication to close off the newest offer.

Guarantee removing can occur in the event the bank proposes to funds a keen amount mainly based solely into equity of your home rather than on the ability to spend. This can lead to skipped payments and you can ultimate foreclosures.

Non-old-fashioned circumstances, such finance having continually expanding monthly payments otherwise low monthly obligations that have a big balloon commission due towards the bottom of one’s loan’s name, is going to be hazardous if you are not on top of the facts.

Mortgage servicer violations can include badly recharged costs, wrong or unfinished membership comments or rewards wide variety, otherwise inability to reveal the rights once the a homeowner.

New do it yourself mortgage cons are present whenever a builder ways that create family improvements or solutions, quoting a good price, then again challenges you on signing up for a home guarantee personal line of credit otherwise loan with a high interest and you will fees.

How HELOCs is paid down

For the mark time of the HELOC, you will end up expected to generate monthly attention-simply costs. Due to the fact mark months ends, you will additionally must initiate paying one outstanding balance toward HELOC.

The most famous type of repayment is by while making monthly installments that can defense each other dominant and attention, such in your first mortgage. When you are your interest only repayments is generally seemingly low, when you begin paying off the main your own monthly obligations will increase considerably.

Consider, the rate on good HELOC can often be varying, so that your monthly payments could possibly get change over date. Before signing into the mortgage records, definitely know very well what the upper cap is found on the newest rate (in many instances it can be of up to 18%) and estimate how higher your own monthly installments can go into the cost several months to make sure you can afford all of them.

Last Updated on December 2, 2024 by Bruce