America’s sensible construction drama was inspired for the high area from the fact that truth be told there are not adequate land in america at this time to meet up with demand. Higher structure can cost you and you can labor shortages imply developers can’t generate timely enough to maintain house creation, and People in the us whom currently own property is actually reluctant to sell an enthusiastic resource that is admiring easily.

It offers pushed home values to help you or past its pre-economic failure peaks, making prospective homeowners as opposed to an easily affordable alternative. If you find yourself there is no simple augment, signals when you look at the federal government recommend you to solution is bringing enhanced attention-manufactured construction.

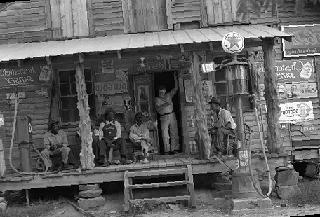

In earlier times named cellular house, are manufactured properties are built in a manufacturing plant, transmitted to help you an internet site . toward a beneficial flatbed vehicle, and attached to-webpages. Never to feel mistaken for prefab belongings, having parts produced in a manufacturer but they are mainly created on-website, manufactured belongings pricing only $forty-five,000, a mere fraction of your average price to have another solitary-nearest and dearest web site-created household off $323,000.

Fannie mae and you will Freddie Mac computer, the government-backed financial facilitators, launched preparations when you look at the January to really make the are available housing marketplace a whole lot more active by buying way more are available property money along side 2nd three ages.

Is are created casing simplicity America’s sensible property crisis?

A couple weeks later on, the latest Agencies out-of Housing and Metropolitan Advancement (HUD) established it absolutely was looking at laws up to are created housing as a result so you’re able to Chairman Trump’s administrator commands to minimize regulations.

From the mid-1990’s, were created houses creation exploded because of the sorts of simple borrowing who does spread through the housing marketplace a great very long time afterwards. However, hop over to the website ever since then, development features plummeted, making affordable houses advocates wondering as to the reasons-of course, if a revival of your markets could help fill the newest eager houses dependence on lowest-earnings family.

There was certainly an inexpensive construction gap which is growing and you will growing and you will growing, said Laurie Goodman, vp of Construction Funds Plan Heart from the Urban Institute. Are made housing is every bit as good as site depending housing most of the time. What makes exactly how many are designed construction equipment maybe not increased so you can in which it actually was just before?

Is actually money carrying right back are built homes?

The complete price tag for a created housing equipment is going become smaller than one having a different webpages-depending family atlanta divorce attorneys situation, but really does that mean a decreased-income family members helps you to save from the choosing a mobile domestic?

Capital a made domestic has gotten harder as 1990’s. Back then, new are designed home financing field is actually controlled from the a friends named Green Tree, which each other started are built mortgage brokers and securitized all of them. More this era, are created construction boomed as basic borrowing flowed for the sector.

However, because of a good confluence out of items, as well as sagging credit conditions you to definitely crept on world, defaults towards are made homes financing piled-up, the securities went boobs, while the marketplace for are made domestic loans folded.

It absolutely was burdensome for the industry to recuperate because the repossessing good are made home is infinitely much harder and you can high priced than just repossessing a great site-oriented family. As a result, Green Forest are ordered less than stress of the Conseco in the 1998. A few of the lenders that adopted Environmentally friendly Tree towards the business ran broke.

Meanwhile, easy borrowing moved out to the website-depending housing marketplace, siphoning people regarding the were created housing industry. So it transition inflated the fresh new houses bubble who would fundamentally bust within the 2008, and the are made housing market hardly ever really recovered. Some pondered if the boom try far more a direct result simple borrowing than actual demand.

Now, cellular property should be classified because sometimes a bona fide house property otherwise your own possessions. Consumers is loans a buy by way of a classic mortgage when your property is categorized since the a property, but some are made home is funded since individual assets with a good chattel loan.

Last Updated on December 7, 2024 by Bruce